Key takeaways

Many law firm expenses may be deductible if they are ordinary, necessary, properly documented, and ultimately paid by the taxpayer rather than reimbursed by a client or employer.

For mileage and travel, proper documentation matters just as much as the expense itself. While regular commuting is not deductible, qualifying business driving and business travel away from your tax home may be deductible.

Some deductions depend heavily on an attorney’s status. W-2 lawyers, partners, and law firm owners may not all get the same result for the same expense.

Keeping clean books, organized receipts, and consistent expense tracking makes year-round tax planning for lawyers much easier.

Running a law firm comes with expenses beyond what many attorneys expect. Payroll, office equipment, software, bar dues, and marketing costs can add up quickly.

That’s why lawyer tax deductions matter. When you understand which expenses may qualify, you can potentially reduce taxable income, keep cleaner books, and avoid missing legitimate write-offs at filing time. In general, the IRS allows businesses to deduct expenses that are “ordinary and necessary” for the trade or business. For law firms, this can include costs such as legal research tools, malpractice insurance, business travel, and practice management software. By contrast, personal expenses, commuting to a regular office, and many entertainment costs are generally not deductible.

It’s important to note that deduction rules can also vary depending on a lawyer’s role and the structure of their practice. Solo practitioners and firm owners may be able to deduct certain business expenses directly on their returns if they qualify as ordinary and necessary expenses for operating a business. The IRS explains that self-employed individuals can deduct qualifying business expenses related to their trade or profession. By contrast, W-2 attorneys generally cannot deduct unreimbursed employee expenses on their federal returns because the Tax Cuts and Jobs Act suspended most miscellaneous itemized deductions, including unreimbursed employee expenses, through 2025 under current law. Future legislation could change this treatment. Partners and attorneys who receive income through a Schedule K-1 may face different considerations depending on how their partnership handles expenses and reimbursements.

Note: This guide is for educational purposes only and is not exhaustive. Tax treatment depends on your facts, your law firm’s structure, and the tax year at issue, so attorneys should work with a CPA or tax advisor before filing.

1. Marketing expense deductions

Law firms need to invest in visibility just like any other business. In many cases, marketing and advertising costs may qualify as law firm tax deductions when they’re directly tied to promoting the practice.

Potentially deductible examples include:

Directory listings such as Avvo and Martindale-Hubbell

Google Ads and paid search campaigns

Social media advertising

Website design, development, and maintenance

SEO services

Printed mailers, brochures, and business cards

Sponsorships that primarily promote the firm’s services and are not political contributions or charitable donations.

A practical note: Not every promotional cost belongs here. Expenses that are personal, political contributions, or primarily entertainment-related may not qualify in the same way. Keep invoices and campaign records so your tax professional can classify them correctly under the IRS ordinary and necessary standard.

2. Retirement and pension plan deductions

Retirement contributions are often one of the most valuable attorney tax deductions, especially for firm owners who want to reduce taxable income while building long-term savings.

Common options include:

SIMPLE IRAs

401(k) plans

SEP IRAs

Other qualified pension arrangements

For 2026, the IRS increased the annual limit for defined contribution plans under IRC §415(c) to $72,000. This includes both employer contributions and employee elective deferrals combined, subject to additional plan-specific rules and compensation limits. Contributions are generally limited to the lesser of 100% of an employee’s compensation or $72,000, depending on plan type and eligibility rules.

This is an area where entity structure matters. A solo attorney, PLLC owner, partnership, or larger firm may each have different deduction mechanics, and plan design affects the result. Also, not every retirement-related payment is deductible in the same way or in the same year, so it’s worth confirming plan-specific rules before year-end.

3. Mileage, vehicle, and local travel deductions

Many lawyers drive for business—court appearances, client meetings, depositions, witness interviews, bank visits, and trips between firm locations. Those miles can add up, making accurate law firm accounting and record keeping important when claiming mileage tax deductions for lawyers.

But one correction is important—commuting from home to your regular workplace is generally not deductible. That’s considered a personal commuting expense, not a business expense. By contrast, qualifying business trips may be deductible if properly documented.

The IRS standard mileage rate for business use of a vehicle is:

70 cents per mile for 2025

72.5 cents per mile for 2026

Lawyers can generally choose between the standard mileage method and the actual-expense method, subject to IRS eligibility rules. If you use the actual-expense method, you need detailed records for gas, oil, maintenance, insurance, repairs, registration, and depreciation or lease costs, allocated between business and personal use. If you use the standard mileage method, you still must maintain a timely mileage log showing the date, destination, business purpose, and miles driven.

4. Travel deductions

Travel deductions go beyond local driving. If an attorney travels away from their tax home for business and the trip is long enough to require sleep or rest, certain travel expenses may be deductible. The IRS generally treats these as ordinary and necessary travel expenses.

Examples may include:

Airfare, train, or bus tickets

Taxi, rideshare, and shuttle fares

Rental car costs

Parking and tolls

Lodging

Shipping or luggage fees

Laundry on a qualifying business trip

Meals while traveling

However, there are limits. Business meals are generally subject to a 50% deduction limit under current federal tax law, and personal sightseeing, extra vacation days, or family expenses mixed into a trip may not qualify. Good records matter here too: save receipts and document the business purpose, destination, dates, and attendees when relevant.

5. Educational expense deductions

Continuing education is part of practicing law responsibly, and in some cases, it may also support tax deductions for lawyers.

Potentially deductible examples include:

CLE courses required to maintain a license

Practice-area training tied to current legal work

Legal conferences with a clear business purpose

Professional development for attorneys and staff

Subscriptions to training platforms

A helpful distinction:

CLE to maintain an existing license or improve current skills is often more likely to qualify as a business expense.

Education expenses are generally not deductible if they qualify the taxpayer for a new trade or business or meet the minimum educational requirements for entering the profession.

Treatment can also vary by role. A law firm owner may deduct qualifying business education differently from a W-2 attorney whose employer pays the cost or reimburses it. For employees, reimbursement arrangements are often key.

For a deeper dive on this, check out our CLE course on Current Trends in Attorneys' Fees.

6. Business supplies and services

Business supplies and services often make up a large share of law firm tax deductions. Some of the most common deductible categories for attorneys include:

Practice management software

Legal research tools like Westlaw, Lexis, and Casetext

Document management services

Accounting and bookkeeping support

E-filing fees and court costs are firm expenses and not treated as reimbursable client advances

Postage, courier, and shipping costs

Office supplies and printer costs

Computers, monitors, scanners, and peripherals

IT support and cybersecurity services

Many modern firms are also investing in tools that support a paperless law office, including digital document management systems, cloud storage, and electronic signature platforms. These technologies can reduce administrative overhead while helping keep business documents organized for tax and compliance purposes.

The key question is usually whether the cost is ordinary, necessary, and truly a firm expense. If a client reimburses the cost, or if an expense is partly personal, the deduction may require different treatment. Maintaining a clear chart of accounts and organized documentation can make it easier to categorize expenses correctly and support lawyer tax deductions during preparation.

7. Home office expenses

The home office deduction can be valuable for solo and self-employed attorneys, but it has strict rules.

Under IRS guidance, the home office must generally be used regularly and exclusively for business and be either the principal place of business, a place used to meet clients in the normal course of business, or a separate structure used for the trade or business. The IRS also allows either the simplified method or the actual-expense method. The simplified method allows a deduction of $5 per square foot of qualifying space, up to 300 square feet.

For lawyers, that means a kitchen table that doubles as family space usually doesn’t qualify. A dedicated office used only for firm work is a much stronger candidate. Hybrid work can make this trickier: If you’re a W-2 attorney who also works from a firm office, federal deduction rules are usually much less favorable than they are for self-employed attorneys.

Coworking expenses may be easier to treat as ordinary office or rental expenses rather than attempting to claim a home-office deduction that does not meet the exclusive-use test. Either way, keep floor plans, expense records, and a clear explanation of how the space is used.

8. Interest on student loans

This section needs a clear distinction: Student loan interest is generally not a business deduction for a law firm. Instead, it may qualify as an above-the-line personal deduction on an individual return if the taxpayer meets the eligibility requirements. The IRS says the deduction is limited to the lesser of $2,500 or the amount of interest actually paid, subject to income phaseouts and other rules.

That makes student loan interest very different from interest on a true business loan, such as a line of credit used for firm operations, which may be deductible as a business expense if it otherwise qualifies. Attorneys should avoid lumping these together.

9. Credit card fees

Payment processing fees are another common law firm tax deduction. If your firm accepts cards as a payment method and pays merchant or processing fees, those costs are often treated as ordinary business expenses.

This matters because card acceptance is now widespread in legal practice. According to the 8am™ 2025 Legal Industry Report, 82% of law firms surveyed accept credit and debit card payments, and 59% say integrating payment processing into billing software leads to faster collections.

Remember, the way your firm handles processing fees can affect how they should be recorded in your books. Firms should ensure their books clearly separate processor fees, earned revenue, and client trust funds, where applicable.

10. Bar dues and professional memberships

Bar dues and certain professional memberships are generally deductible business expenses for attorneys when they’re directly tied to practicing law.

Examples may include:

State bar dues

Local bar association memberships

Practice-area section memberships

Inns of court or similar professional organizations

Trade publications and professional subscriptions

Not every membership cost belongs here, though. In general, the IRS doesn’t allow deductions for dues paid to clubs organized for business, pleasure, recreation, or other social purposes. So a country club, dining club, or social club fee is a different story from a state bar membership.

For W-2 attorneys, the federal treatment of unreimbursed dues may differ from that for self-employed attorneys or firm owners.

11. Malpractice insurance and professional liability

Insurance is another category lawyers shouldn’t overlook. Premiums for malpractice and other business-related insurance are commonly treated as ordinary and necessary costs of operating a law practice.

Potentially deductible examples include:

Professional liability insurance premiums

Tail coverage

Cyber liability insurance

General business insurance

Property coverage for office contents

Certain workers’ compensation insurance or other business-related insurance policies

For example, if a small firm carries malpractice coverage, cyber coverage for client data, and a general liability policy for its office, those premiums are usually much more likely to be treated as deductible business expenses than personal insurance policies. As always, mixed-use or personally benefiting coverage should be reviewed carefully with a tax advisor.

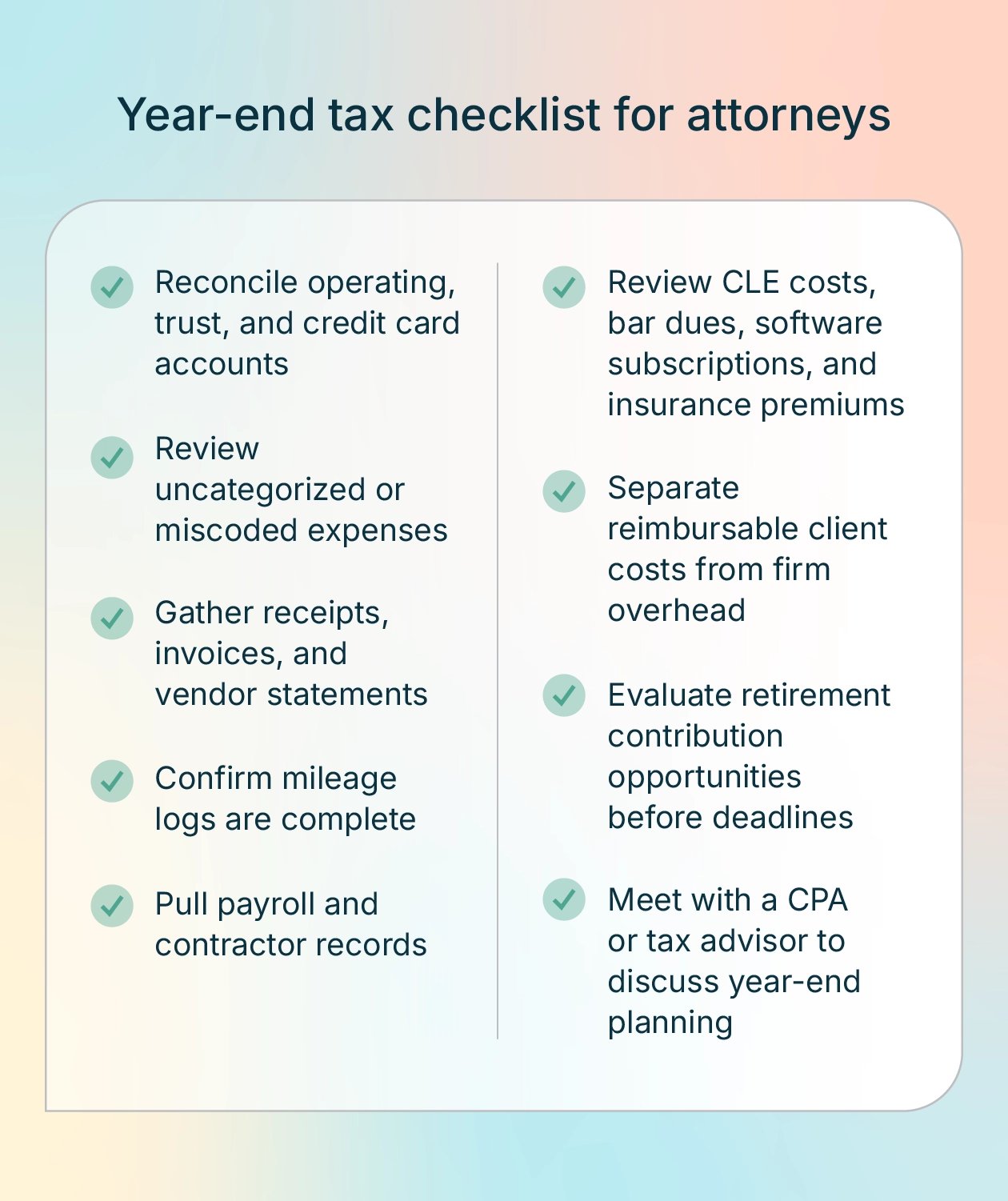

Year-end tax checklist for attorneys

The best time to prepare for tax season is before year-end, while the records are still easy to review and fill in.

A simple year-end checklist for attorneys includes:

Reconcile operating, trust, and credit card accounts

Review uncategorized or miscoded expenses

Gather receipts, invoices, and vendor statements

Confirm mileage logs are complete

Pull payroll and contractor records

Review CLE costs, bar dues, software subscriptions, and insurance premiums

Separate reimbursable client costs from firm overhead

Evaluate retirement contribution opportunities before deadlines

Meet with a CPA or tax advisor to discuss year-end planning

Lawyers often overlook attorney tax deductions tied to CLE, bar dues, software subscriptions, payment processing fees, and professional services, especially when those costs are scattered across multiple systems or paid late in the year.

Streamline business expense tracking to manage taxes efficiently

Knowing which tax deductions for lawyers may apply is only part of the equation. The other part is keeping clean, consistent records throughout the year.

When attorneys can clearly track expenses tied to marketing, travel, education, software, insurance, and office operations, they’re in a better position to potentially reduce taxable income and avoid missing legitimate lawyer tax deductions. Accounting and expense management tools can help by organizing transactions, storing receipts, categorizing expenses, and producing reports that make tax preparation easier for both firms and accountants.

For firms using 8am, both MyCase and LawPay offer integrated solutions that provide this level of financial visibility. Learn more about 8am today—book a demo.

Lawyer tax deductions FAQs

What documentation is required to claim business mileage for court visits and client meetings?

The IRS expects timely, adequate records showing the date, business purpose, starting point, destination, and miles driven for each business trip. A contemporaneous mileage log or reliable digital mileage tracker is the strongest support. It also helps to keep related backup, such as court calendars, client meeting confirmations, or matter notes.

What is the most overlooked tax deduction for lawyers?

It often depends on the firm's structure, but some of the most commonly missed items include retirement plan contributions, bar dues, CLE expenses, software subscriptions, payment processing fees, and properly documented business travel or meals. Owner-level planning can be especially valuable because retirement funding and year-end timing decisions may materially affect taxable income.

How does the home office deduction apply to lawyers who also work at a firm office or in court?

A lawyer can generally claim a home office deduction only if a specific area of the home is used regularly and exclusively for business and the space meets the IRS principal-place-of-business or client-meeting test. Having other work locations doesn’t automatically disqualify the deduction, but W-2 employee treatment is far less favorable than self-employed treatment. The simplified method remains available at $5 per square foot for up to 300 square feet.

Can MyCase help track deductible expenses and generate tax‑ready financial reports for my firm?

Yes. MyCase can help firms centralize billing, payments, and accounting data, making year-end reconciliation and reporting more manageable. When paired with LawPay and 8am spend management workflows, firms can keep a closer track of operating activity, payment-related costs, and the records their accountant may need for tax preparation.