Accepting credit card payments is a routine part of doing business for most professional service firms, but not all payment processing setups are the same. Whether you’re sending invoices, collecting payments, or managing recurring charges, the processing model you choose has a direct impact on cash flow, profitability, and the reliability of your payment system.

Two of the most common options for payment processing are dedicated merchant accounts and payment aggregators. While both enable your business to accept credit cards, they are built on very different account structures. Those differences influence how your account is approved, how quickly funds are deposited, how risk is managed, and how much visibility and control you have over payment activity.

This guide explains how each model works and how to evaluate which approach aligns with your firm’s size, transaction volume, and risk profile. If you’re reassessing your payment setup, comparing providers, or evaluating payment aggregator pros and cons, understanding this distinction will help you make a more informed decision.

Payment aggregator vs. merchant account: Definitions and how they work

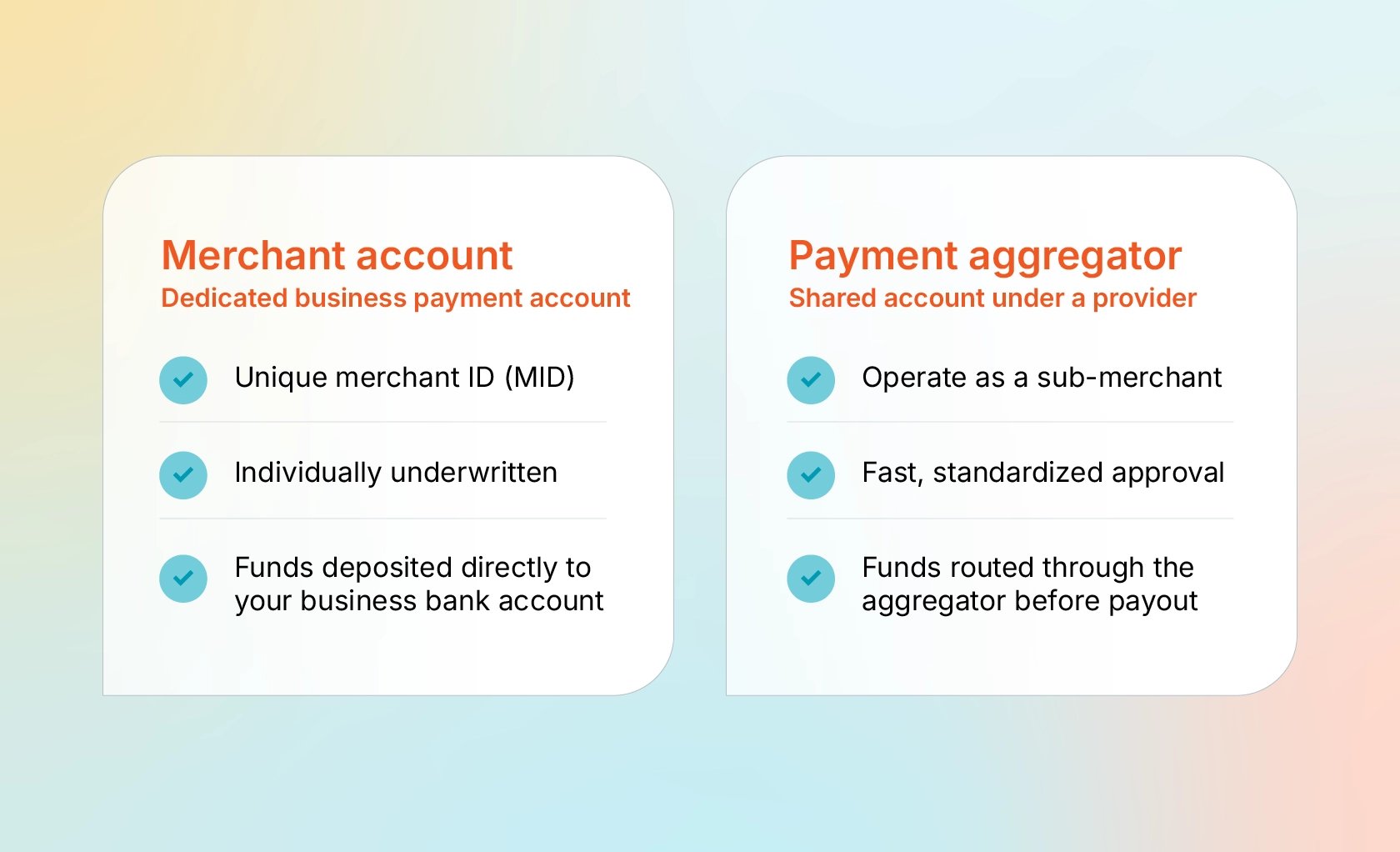

A merchant account is a dedicated account opened in your business’s name through a payment processor. When the processor approves your account, your firm receives its own unique merchant identification number (MID), which is used to route and track your transactions.

This account acts as a holding point between your client’s card issuer and your business bank account, allowing credit card payments to be authorized, settled, and deposited. Because the account belongs specifically to your firm, it is underwritten based on your business profile, transaction history, and risk level.

A payment aggregator, also called a payment facilitator or payfac, is a type of payment processor that allows businesses to accept card payments as a sub-merchant under the aggregator’s master account. Several providers, including Stripe, Square, and PayPal, use this model.

The aggregator oversees the primary merchant account and the underwriting process, enabling businesses to start accepting payments quickly without applying for their own individual merchant account. Transactions are still processed in the firm’s name, but they are ultimately managed within the aggregator’s account.

Account setup

If you’re interested in setting up a private merchant account, your business must be vetted through a “know your customer” (KYC) underwriting process. This review is required under federal regulations designed to prevent money laundering and fraud.

During underwriting, the bank or payment processor evaluates factors such as how long your business has been in operation, its financial stability, the owner’s credit profile, and documentation confirming the legal connection between the owner and the business.

The merchant account provider will also ask detailed questions about how your firm accepts payments, including typical transaction sizes, billing frequency, and client locations. This information helps configure your account appropriately from the start. Once approved, your firm has a dedicated merchant account tailored to your specific payment patterns and risk profile.

With a payment aggregator, onboarding is typically faster because there is no individual underwriting process for each business. Instead, providers approve businesses under their master merchant account, often through a short online application.

However, because the aggregator has not conducted a detailed review of your firm upfront, it relies on standardized onboarding and broad risk controls across its entire customer base. This streamlined approach makes setup faster, but it also means your account is not tailored to your firm’s specific payment patterns in the same way as a dedicated merchant account.

Processing volume

Another key difference between merchant accounts and payment aggregators is the volume of payments your firm can process without delays or interruptions.

With a dedicated merchant account, the processor reviews your expected transaction volume during underwriting. Your provider will ask about your typical monthly volume, average transaction size, and any seasonal spikes. This allows you to establish appropriate processing thresholds (sometimes called volume limits) in advance and, in some cases, adjust them as your business grows. As a result, higher-than-average activity is less likely to trigger concern if it falls within the agreed-upon range.

Payment aggregators operate differently. Instead of setting individualized volume expectations, they manage risk across their entire base of sub-merchants. Your firm processes payments under the aggregator’s master account, alongside many unrelated businesses.

If your transaction volume suddenly increases or deviates from typical patterns—which can occur in peak processing months—the aggregator may impose temporary holds or limits while the activity is evaluated.

Fee structure

Merchant accounts and payment aggregators use different pricing models, and those differences can affect your costs over time.

With a merchant account, fees are typically set during underwriting. Your provider may adjust pricing based on your transaction volume, average payment size, industry, and processing history. Many merchant accounts use interchange-plus pricing, which includes the card network’s base fee (1.5% to 2.5%), a small processor markup (0.2% to 0.5% plus 10 to 15 cents per transaction), and a $10 to $30 monthly fee. This model offers transparency and can lower costs as your volume grows.

Payment aggregators usually rely on flat-rate pricing. Providers commonly charge around 2.9% plus 30 cents per online transaction, with no monthly account fee. That simplicity can be appealing, but flat-rate pricing is often more expensive at higher volumes, which can increase costs as your firm grows.

Payment processors often point to about $10,000 per month in card payments as a benchmark when evaluating pricing models. Firms below that threshold may benefit from the simplicity of an aggregator, while those above it can often reduce fees with a merchant account.

Processing time

With a dedicated merchant account, funds are typically deposited into your business bank account within one to two business days after a transaction is processed. Some payment aggregators offer similar timelines. However, in certain situations, transfers can take longer, particularly if the aggregator delays settlement or requires additional review before releasing the funds.

In addition, payments processed through an aggregator are first deposited into your account with the payment facilitator, not your business bank account. You may then need to manually transfer those funds to your bank, depending on the provider’s payout schedule. Also, when your funds are in the aggregator account, they typically don’t have the same Federal Deposit Insurance Corporation (FDIC) protections as funds deposited into your business bank account.

Fraud prevention

Because payment aggregators onboard businesses quickly and manage risk across a large pool of sub-merchants, they often rely on automated fraud-detection systems to monitor transactions. If activity appears unusual, the aggregator may delay payouts, place a temporary hold on funds, or restrict the account while it conducts a review. In some cases, accounts can be suspended or closed if the provider determines that the activity violates its terms or risk policies. These actions are intended to limit fraud exposure, but they can disrupt access to funds that have not yet been transferred to the business’s bank account.

With a dedicated merchant account, fraud monitoring is typically based on your firm’s individual profile and transaction history. Because the provider has already completed a detailed underwriting review, it has more context about your normal payment patterns. If suspicious activity occurs, the processor will often contact you to investigate and resolve the issue. While restrictions can still happen, this individualized approach can make it easier to address concerns and avoid disruptions to payment processing.

Customer service

Customer service is another important consideration when selecting a payment processing model. Because payment aggregators support large numbers of businesses under a shared account structure, assistance is usually provided through centralized support teams. This can make it harder to get help that reflects your firm’s specific situation.

Merchant account providers often take a more individualized approach. When your business has its own merchant account and completes thorough underwriting, the provider has a clearer understanding of your transaction patterns, billing model, and risk profile. This allows support teams to offer more relevant guidance, respond more efficiently to questions, and help address issues in line with how your firm operates.

Choose the right payment model for your firm

Merchant accounts and payment aggregators both make it possible to accept credit card payments, but they differ in how they handle risk, pricing, and long-term scalability. For professional services firms, the payment processing model you use can influence everything from processing costs to account stability and the level of support you receive as your business grows.

8am™ provides payment solutions built specifically to help professional services firms accept payments efficiently and gain clearer visibility into their finances:

LawPay is a legal billing and payments solution that allows law firms to accept secure online payments, simplify billing, and stay compliant with trust accounting rules with tools designed for legal workflows.

CPACharge gives accounting professionals the ability to streamline invoicing, get paid faster, and manage client payments more efficiently.

ClientPay helps architecture, engineering, and construction firms collect client payments securely, improve cash flow, and support complex billing arrangements common in project-based work.

To see how 8am can support your business with reliable payments and dedicated service, book a demo today.